Figures for the final quarter of 2020 newly published in the BMF’s Builders Merchants Building Index (BMBI) confirm the sector’s continued bounce back from the April lockdown which led to a dramatic decline in sales during Q2.

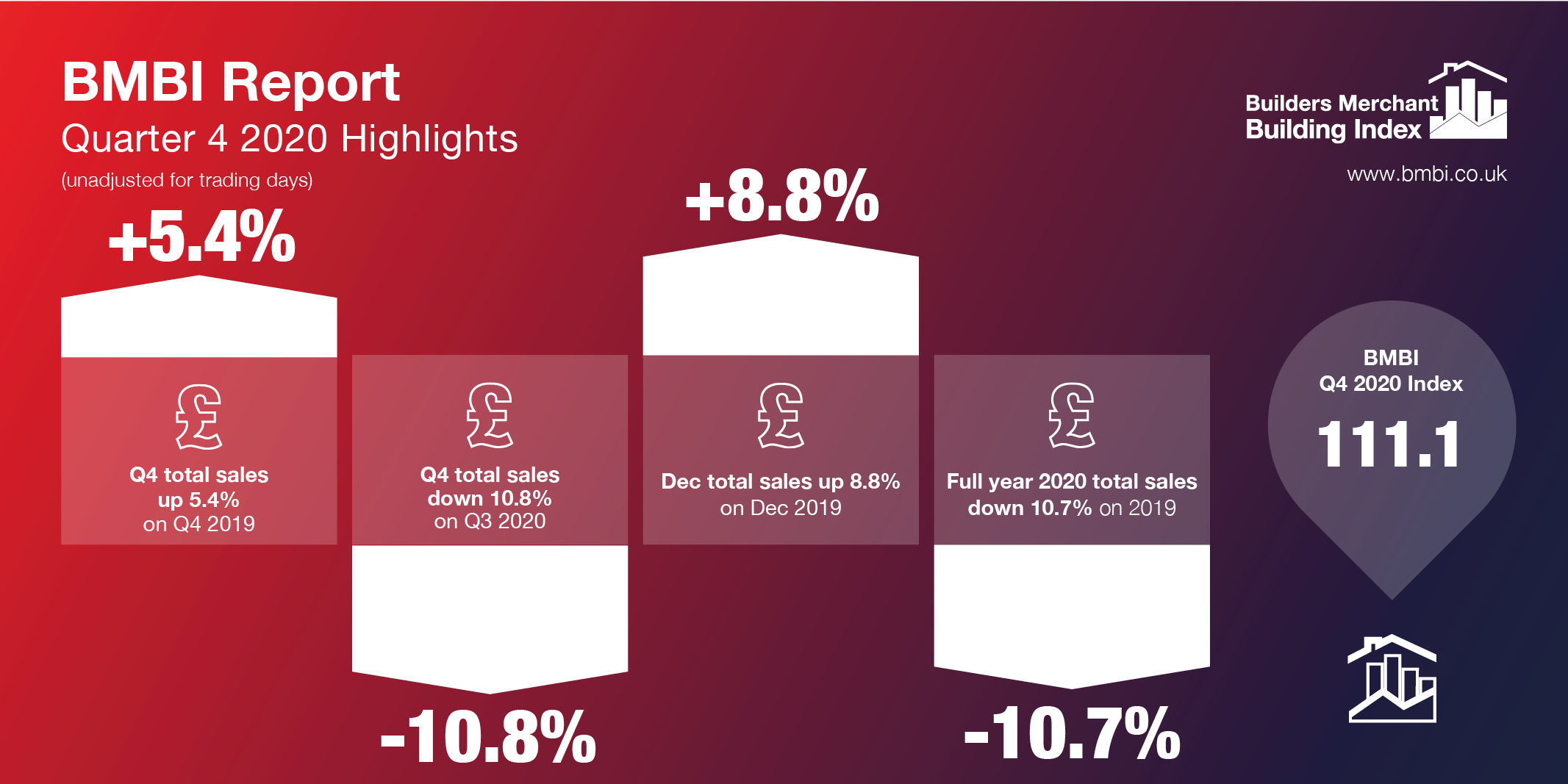

The BMBI had previously reported a strong performance in Q3 with sales returning to near normal levels. The positive trend continued in Q4 2020, with total builders’ merchants’ sales growth of +5.4% compared with Q4 2019, helped by one more trading day this year.

The Q4 year-on-year increase was driven by strong performances in Landscaping (+22.9%), Timber & Joinery (+12.7%) and Heavy Building Materials (+4.3%). Sales value growth in Timber & Joinery was predominantly driven by Timber, with the well documented stock shortages a key driver. No other product category sold more in Q4 2020 than Q4 2019, with Plumbing, Heating and Electrical (-6.0%) the lowest performer.

There is normally a seasonal sales decline in Q4 and 2020 was no exception. With five fewer trading days in Q4, total builders’ merchants’ sales were down by -10.8% compared to Q3 2020. The average sales a day figure for Q4 (-3.4%) was also down on Q3.

Taking 2020 as a whole, total sales value was down by -10.7% on 2019. Given the public’s focus on their gardens during the first lockdown, it is no surprise that Landscaping was the only category to show an annual increase in sales value (+5.4%), with Workwear and Safetywear (-0.1%) the next best performer. The weakest annual results were found in the more lightside oriented categories with Tools (-20.2%), Plumbing, Heating & Electrical (-19.1%), Kitchens & Bathrooms (-18.1%) and Decorating (-16.5%).

Commenting on the Q4 sales data, John Newcomb, BMF CEO said: “Given widespread site closures both at the start of the pandemic and for extended Christmas shut down periods, the continued year-on year growth seen in the final quarter of 2020 provides a positive indicator of the building industry’s recovery.

“No doubt the Covid effect, including its impact on product availability, will be felt for some time to come. But the adaptability to enforced changes demonstrated by merchants and their trade customers over the past 12 months gives me a cautious degree of optimism for the coming year.”

Emile van der Ryst, Senior Client Insight Manager – Trade at GfK added: “A final review of this year highlights just how well the sector has bounced back. During Q2 the economic outlook for the remainder of 2020 seemed perilous, but a combination of RMI activity plus relaxed restrictions in Q3, followed by Brexit uncertainty combined with anticipated stock shortages in Q4 turned the ship.

“Taking all the above into consideration the final annual result of a -10.7% value declines seems a lot more palatable. 2021 now provides a realistic hope of a return to normality and an expected economic upswing.”