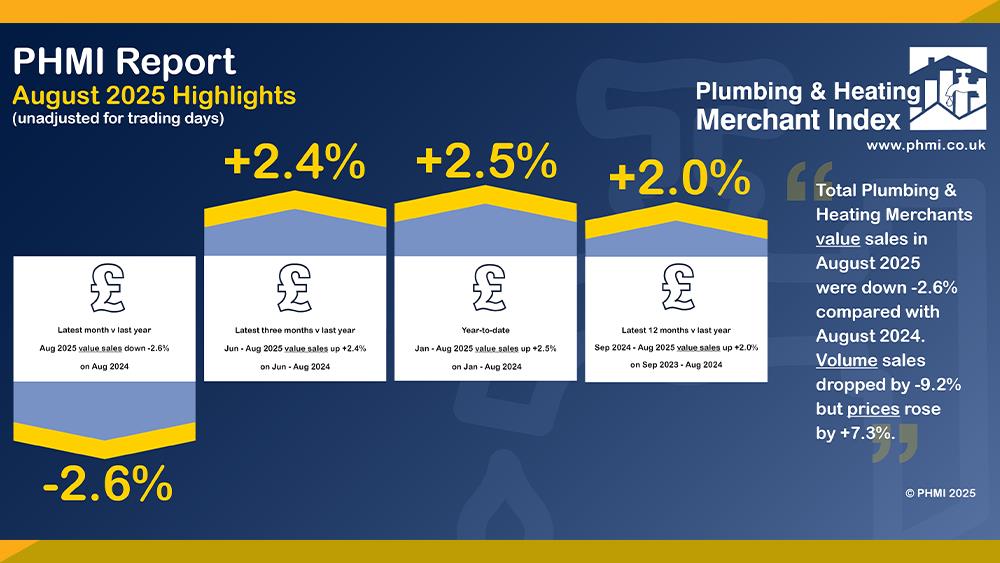

The signs of recovery continue with year-to-date sales up 26.1% in January to April 2021 compared to the same four months last year, with one less trading day.

The latest Plumbing & Heating Merchant Index report published in June shows that value sales through specialist plumbing & heating merchants’ in April were up 192.4.% on April 2020, with merchants selling almost three times as much as the previous year.

The signs of recovery continue with year-to-date sales up 26.1% in January to April 2021 compared to the same four months last year, with one less trading day.

However, with many merchant branches closed last April because of the pandemic, comparisons between 2021 and 2020 are less meaningful. Comparing sales with 2019 and normal trading conditions are more useful. On this basis, value sales through specialist plumbing & heating merchants in April 2021 were up 4.3% compared to April 2019, with no difference in trading days, confirming the strength of recovery in this sector.

Despite a difficult start to the year with a third national lockdown, sales from February to April were 6.6% up on the same period in 2019, with two more trading days.

Month-on-month, value sales were 13.8% below March 2021, not helped by three fewer trading days in April. Average sales a day were just 0.9% lower.

Total sales in the 12 months May 2020 to April 2021 were almost identical to the same period a year earlier (+0.1%), with no difference in trading days.

April’s PHMI Index was 101.8. The average Index over the last three months (February to April) is 107.5, showing an improvement on the previous three months (98.1).

Don Nisbet, Head of Insight, Wolseley, one of the leading plumbing and heating merchant contributors to the PHMI, said: “April saw year-on-year comparisons distorted by last year’s semi closedown so the two-year comparisons are a more useful guide to the state of the market than the spectacular one-year figures. On a two-year comparison, with a more normal 2019, the index is up 4.3% on a monthly basis and up 6.6% on a three-month basis, indicating underlying market growth.

“The coldest April since 1922 will certainly have helped the demand for the boiler and heating market.

“Likewise, the working at home phenomena and the mini housing boom that has flowed from this, and the stamp duty holiday are certainly helping the domestic Plumbing & Heating markets. However, commercial P&H customers will be seeing the flipside impact of the pandemic on the office market. The P&H market is undoubtedly moving in the right direction in terms of demand helped by the short-term boost of the housing market but, looking ahead, there is still a lot of uncertainty over the rest of the year with customer concerns over future availability and prices.”

The Plumbing & Heating Merchant Index is the first to analyse point of sales data collated from a range of specialist plumbing & heating merchants with combined annual sales of £3 billion, to chart their performance month-to-month.

Based on data from GfK’s Plumbing & Heating Merchant Panel, which represents over 80% of the market by value, the report provides reliable data and a platform and voice for the industry, as well as for leading plumbing & heating brands. It is produced by MRA Research for the Builders Merchants Federation. There is no overlap or double counting between PHMI and the Builders Merchants Building Index sales data.

To download the latest report, or learn more about becoming an Expert, speaking on behalf of your market, visit www.phmi.co.uk.